Lucky Mister KYC and Verification: Documents, Checks and Withdrawal Holds

Lucky Mister KYC is not a small box to tick after a win. The official terms reviewed describe age, identity, address, payment-method and source-of-funds checks, and they say withdrawals may be restricted during verification. They also require deposits to come from payment methods in the player’s own name and describe extra AML checks around suspicious transactions. For UK readers, the key point is not that Lucky Mister follows the same local process as a British licensed operator. No Gambling Commission listing for Lucky Mister was found when the UKGC public register was consulted for this guide. The useful answer is narrower: if you register or deposit, assume verification can affect account access and withdrawal timing, prepare only truthful and current information, and do not rely on any review that calls the site no-KYC, anonymous or document-free.

Table of Contents

- What Lucky Mister can ask to verify

- Document categories in the official terms

- Why payment ownership is central

- Withdrawal holds during verification

- Source-of-funds checks are not the same as ordinary ID

- How this differs from UKGC financial vulnerability checks

- Privacy and document caution

- When KYC should make you pause

- KYC FAQ

- Bottom line

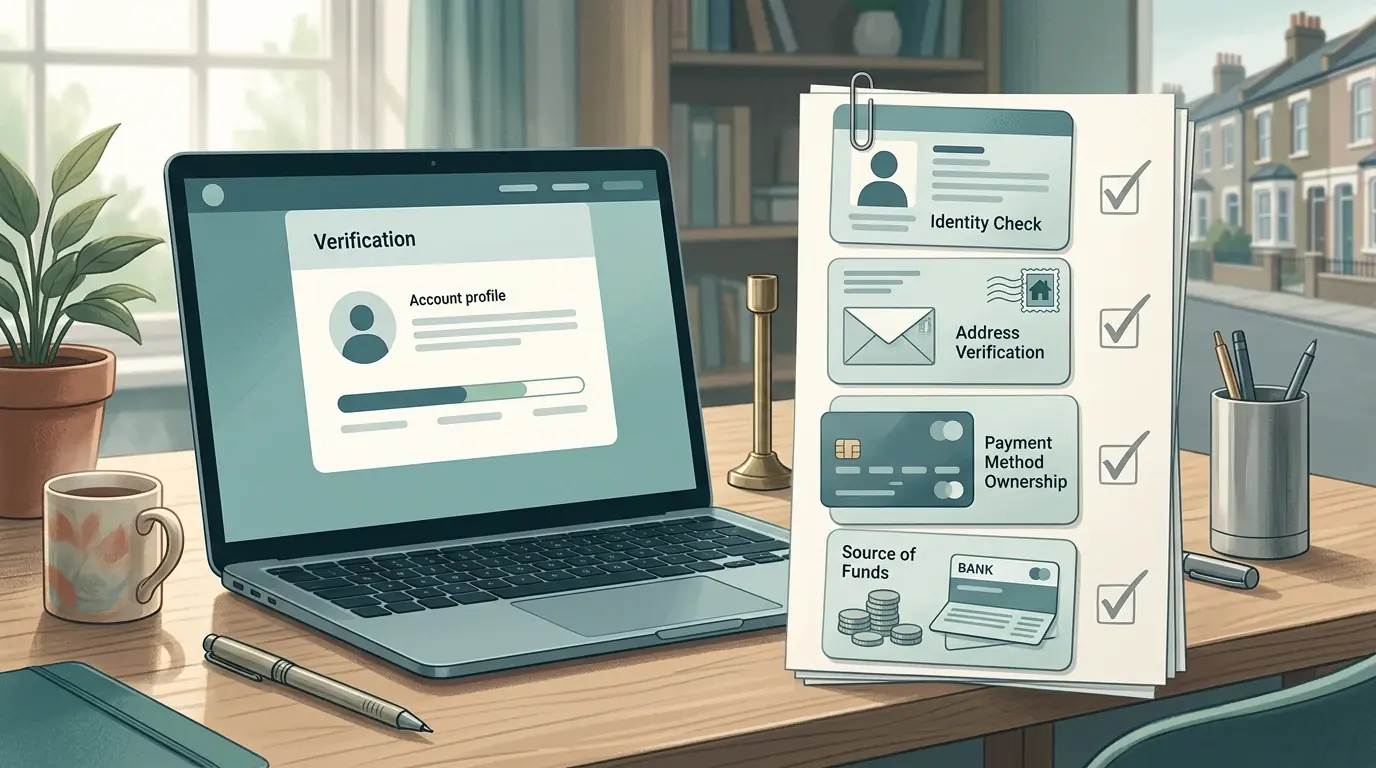

What Lucky Mister can ask to verify

The official terms give several document and data categories. They include identity proof, address proof, payment-method ownership evidence, transaction checks and, in some circumstances, information about source of earnings. The terms also say verification may be done electronically, verbally over the phone, or by requesting documentation. That is a broad compliance power, so public content should not describe the account as anonymous or verification-free.

For a UK reader, the practical issue is timing. A player may not feel the weight of these rules at registration or deposit, but the terms connect verification directly to withdrawal access. If the account name, payment owner, phone number, email address or address record is wrong, the problem can surface when money is already involved.

Document categories in the official terms

| Category | Examples supported by the terms | Why it matters before withdrawal |

|---|---|---|

| Age and identity | Passport, driving licence or ID. | The terms prohibit under-18 use and allow age and identity checks. |

| Address | Utility bill or bank statement showing name and address, with mobile phone bills excluded in one clause. | A mismatch between account address and proof can slow or prevent verification. |

| Payment ownership | Card copies with only permitted card digits visible, CVV hidden, or bank statements showing relevant transactions. | Deposits are required to come from a payment method in the player’s own name. |

| Source of funds or earnings | A declaration and supporting documents such as bank statements or payroll records may be requested. | Extra checks can be triggered when transactions require closer review. |

| Contact and profile data | Email, phone number, name, date of birth and profile information. | Withdrawal wording refers to complete profile and verified contact requirements. |

Why payment ownership is central

Lucky Mister’s terms say third-party funds are not accepted and deposits should be made from accounts, systems or cards registered in the player’s own name. This is not just a deposit detail. It connects to withdrawal routing, document checks and AML review. If a card, wallet or account belongs to someone else, the issue may not appear until the site asks for proof.

The safest reading is simple: do not use another person’s payment method, even with permission. Do not register under a name that does not match the payment method. Do not assume a family member’s card, shared account or borrowed wallet will be treated as harmless. The payment ownership rules page covers the cashier caveats in more detail, but the KYC point is that ownership evidence can be part of verification.

Withdrawal holds during verification

The official rules state that the possibility of withdrawing funds may be restricted during the verification process. That is one of the most important lines for anyone comparing Lucky Mister reviews. A headline processing time is less useful if the account has unresolved KYC, unclear payment ownership or an incomplete profile.

There is also a 3x deposit turnover rule in the verified material. That is separate from identity checks, but it can sit in the same withdrawal queue from the player’s point of view. A withdrawal may be delayed because the player has not turned over the deposit, because the payment method needs checking, because documents are incomplete, or because a transaction review is open.

Use the withdrawal review if your main question is payout timing. This page is narrower: it explains why KYC readiness should be checked before the first deposit, not after a cashout request.

Source-of-funds checks are not the same as ordinary ID

Identity and address proof answer who you are and where you can be linked. Source-of-funds or source-of-earnings evidence answers where money came from. The official terms say Lucky Mister may request information about source of earnings in certain circumstances, including supporting documents such as bank statements and payroll records. This is more intrusive than uploading a passport, so it should be considered before depositing meaningful sums.

The public page should not tell readers how to avoid or game these checks. It should encourage truthful, consistent records and a pause if the player cannot explain the origin of funds. If a request arrives, use only official account channels and do not send documents to third-party reviewers, affiliates or unofficial social accounts.

How this differs from UKGC financial vulnerability checks

UK-licensed operators in Great Britain are subject to an evolving player-protection framework that includes financial vulnerability checks at defined net-deposit thresholds. That is local regulatory context for UK-licensed businesses. It should not be presented as proof that Lucky Mister runs the same UKGC process, because no UKGC licence was verified for Lucky Mister in this research.

The distinction matters. Lucky Mister’s own terms can describe KYC, AML, payment and withdrawal checks, while UKGC rules describe obligations for licensed operators serving British consumers. A cautious UK reader should keep both ideas separate: one is the brand’s account terms, the other is the local regulatory benchmark that helps explain why verification and affordability topics are sensitive.

Privacy and document caution

Verification involves personal information. A player may be asked for identity evidence, address proof, payment documents or source-of-funds records. This page is not legal advice, but it is fair to say that document sharing should be limited to official, current account channels and only when the request is genuine and necessary. Keep copies of what you send, when you sent it and which account screen or message requested it.

Do not upload more information than requested just because a review page suggests it. Do not send documents through social media or to a site that is not the official account area. Do not hide required information in a way that makes the document unusable, but do protect details that the official instructions tell you to cover, such as a CVV code on a card copy.

When KYC should make you pause

- You cannot prove that the payment method is in your own name.

- Your account name, date of birth or address does not match your documents.

- You are relying on a review that calls Lucky Mister anonymous or no-KYC.

- You cannot access the email or phone number connected to the account.

- You are trying to work around a self-exclusion, gambling block or loss-of-control warning.

- You do not understand why a source-of-funds request might be made.

If the issue is registration data rather than documents, read the registration guide. If gambling controls or self-exclusion are involved, stop the account process. GAMSTOP should be presented as a self-exclusion tool for gambling websites and apps run by GB-licensed businesses, not as a topic for workarounds.

KYC FAQ

Is Lucky Mister a no-KYC casino?

No. The verified terms support KYC, document checks, payment ownership checks and possible withdrawal restrictions during verification.

Can Lucky Mister ask for source-of-funds evidence?

Yes. The terms say information about source of earnings and supporting documents may be required in certain circumstances.

Does UKGC financial vulnerability checking prove Lucky Mister’s process?

No. UKGC checks are local context for licensed operators in Great Britain. They should not be presented as Lucky Mister’s process unless directly verified.

What is the safest preparation before depositing?

Use truthful account details, keep payment methods in your own name, check the current terms and be ready to prove identity, address and payment ownership if asked.

Bottom line

Lucky Mister KYC should be assessed before money is deposited. The official terms support identity, address, payment-method, source-of-funds and withdrawal-verification checks. They do not support claims of anonymous play, document-free accounts or guaranteed instant withdrawals. If a UK reader cannot meet those checks, or cannot confirm the wider availability and licensing caveats, the safer decision is to pause.

Prepared by the Lucky Mister Casino editorial staff.